Equity Waterfalls Explained in Layman’s Terms

There are many key terms in commercial real estate that sound esoteric and confuse many beginning investors entering the space. For an exhaustive glossary of important terms, we have you covered. See here.

Today’s key term that we are breaking down: Equity Waterfall

This blog is a collaboration between StackSource teammates Justin Galante, Garet Abrams, and Huber Bongolan to offer you a fresh perspective on what equity waterfalls are and why they matter to you.

“Just as a fisherman must watch the ebb and flow of the tides, an investor and businessperson must be keenly aware of the subtle shifts in cash flow.” - Robert Kiyosaki

Topic Preview

At its core, the waterfall structure describes how cash flows are distributed between partners/owners of the real estate.

Most commonly used by private equity firms, an equity waterfall is a method for distributing cash flow returns among a group of investors.

All equity waterfalls are different and the partnership agreement will outline each deal’s specific investment structure.

Background

At its core, the waterfall structure describes how cash flows are distributed between partners/owners of the real estate. The partners are broken down between Limited Partners (LPs) and General Partners (GPs).

LPs are usually passive investors, with typically no involvement in the day-to-day operations. Keeping it simple, the LPs just provide the cash. On the other hand, the GPs take a more active role and are responsible for managing the daily business operations.

Definition

Most commonly used by private equity firms, an equity waterfall is a method for distributing cash flow returns among a group of investors.

Analogy

You can think of a waterfall in which the water (cash flows) flows into different cups stacked in a pyramid. As the cups at the top are filled, the remaining water spills over and fills the cups below, and this repeats until the water runs dry. These cups of water (cash flow) are then distributed to the GP’s and LP’s depending on what tier they’re in.

To put it a different way, filling of the first top glass represents the end of the 1st tier in the waterfall structure. Once the Tier 1 hurdle is met, the water spills over, the water (remaining cash flow) moves onto the 2nd tier, which usually has a different equity distribution. Each tier does not necessarily distribute equity to the GP and LP at the same rate. Depending on the structure agreement, each tier can distribute equity at different rates.

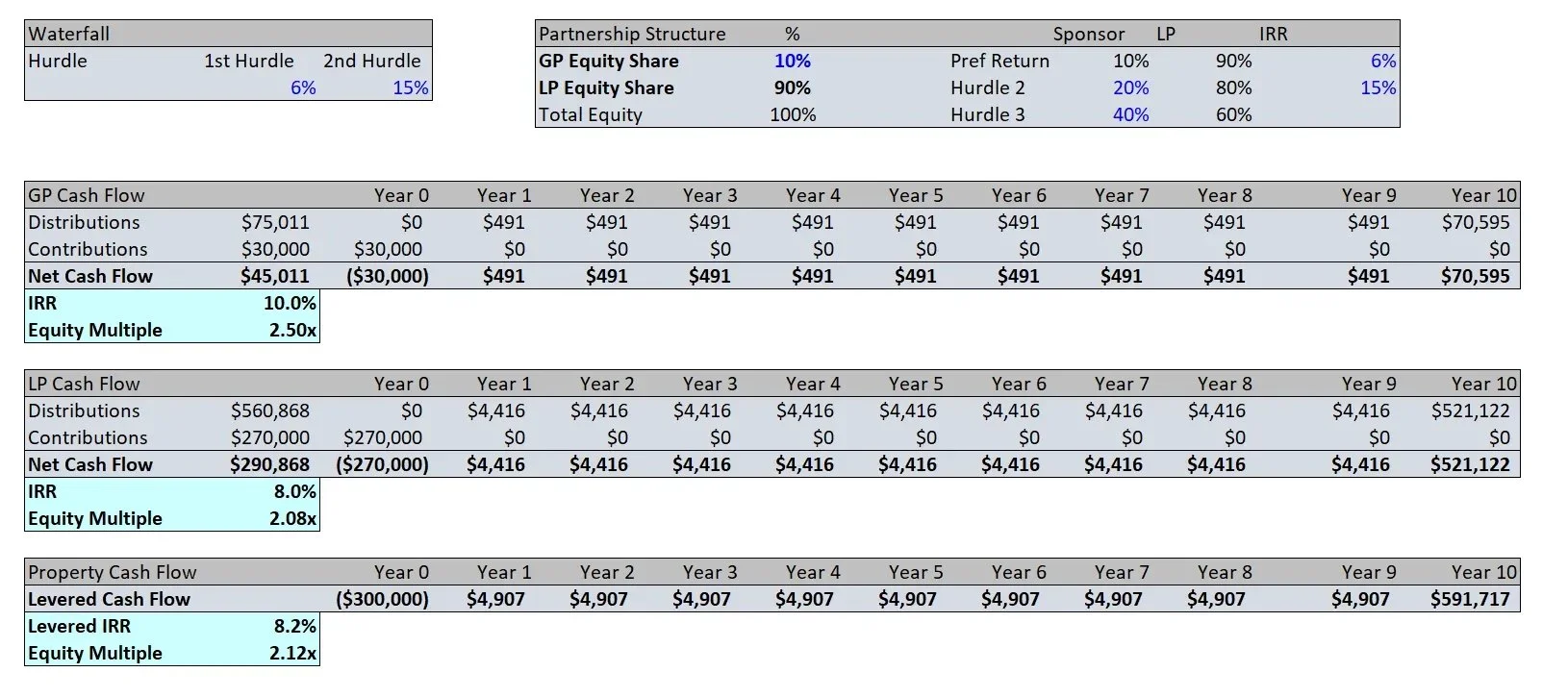

Waterfall Example

In this example, this equity waterfall is broken down into 3 tiers.

Let’s assume that LPs contributed 90% of the equity and GPs contributed 10%.

Tier 1: cash flow is disbursed to investors pro rata until they have recovered their initial capital contribution and preferred return rate of 6% is paid out.

Tier 2: remaining cash flow is distributed 80% to LPs and 20% to GPs until a 15% IRR hurdle is met.

Tier 3: cash flows above that 15% IRR hurdle are disbursed 60% to LPs and 40% to GPs for all remaining cash flows

Now let’s add hypothetical dollar values to this waterfall cash flows example.

Assumptions:

Purchase Price $1,000,000

Debt: $700,000 (70% LTC, 5% rate, 30-year amortization)

Equity: $300,000

Limited Partner (LP) Split of Equity: $270,000 (90% Contribution)

General Partner (GP) Split of Equity: $30,000 (10% Contribution)

Net Operating Income (NOI): $50,000 (5% Capitalization Rate — Untrended)

Exit Cap Rate: 4.5%

(Project-level IRR is sub-10% because this example is a stabilized cash flowing asset. Value-Add plays typically yield 13–16% IRR and construction deals typically yield 20%+ IRR)

Disclaimer

All equity waterfalls are different and the partnership agreement will outline each deal’s specific investment structure. Some waterfalls have dozens of complicated hurdles and provisions, but the overall hierarchy and concepts remain somewhat the same. GP’s will typically receive a larger percentage of the total cash flows upon reaching higher hurdles.